“We recommend the

linking of pay with productivity, with a simultaneous focus on technology,

skill and incentives. We recommend that Pay Commissions be designated as ‘Pay

and Productivity Commissions’, with a clear mandate to recommend measures to

improve ‘productivity of an employee’, in conjunction with pay revisions.We

urge that, in future, additional remuneration be linked to increase in

productivity.” – 14th Finance Commission

“We recommend the

linking of pay with productivity, with a simultaneous focus on technology,

skill and incentives. We recommend that Pay Commissions be designated as ‘Pay

and Productivity Commissions’, with a clear mandate to recommend measures to

improve ‘productivity of an employee’, in conjunction with pay revisions.We

urge that, in future, additional remuneration be linked to increase in

productivity.” – 14th Finance Commission

14th Finance

Commission’s recommendations related to Pay Commission, Salary, Pension:- Recommendations

x. We reiterate the

views of the FC-XI for a consultative mechanism between the Union and States,

through a forum such as the Inter-State Council, to evolve a national policy

for salaries and emoluments. (para 17.28)

xi. We recommend the linking of pay with productivity, with a simultaneous

focus on technology, skill and incentives. We recommend that Pay Commissions be

designated as ‘Pay and Productivity Commissions’, with a clear mandate to

recommend measures to improve ‘productivity of an employee’, in conjunction

with pay revisions.We urge that, in future, additional remuneration be linked

to increase in productivity. (para 17.29)

xii. We urge States

which have not adopted the New Pension Scheme so far to immediately consider doing

so for their new recruits in order to reduce their future burden. (para 17.30)

Recommendations –

Public Expenditure Management

118. We reiterate the

views of the FC-XI for a consultative mechanism between the Union and States,

through a forum such as the Inter-State Council, to evolve a national policy

for salaries and emoluments.

119. We recommend the

linking of pay with productivity, with a simultaneous focus on technology,

skill and incentives. We recommend that Pay Commissions be designated as ‘Pay and

Productivity Commissions’, with a clear mandate to recommend measures to

improve ‘productivity of an employee’, in conjunction with pay revisions. We

urge that, in future, additional remuneration be linked to increase in

productivity. (para 17.29)

120. We urge States

which have not adopted the New Pension Scheme so far to immediately consider

doing so for their new recruits in order to reduce their future burden. (para

17.30)

14th Finance

Commission’s detail report related to Pay Commission, Salary, Pension:- Fiscal

Deficit

3.4 The fiscal deficit

of the Union Government relative to GDP declined steadily from 6.1 per cent in

2001-02 to 4.5 per cent in 2003-04. The FRBM Act mandated reducing the fiscal

deficit to 3 per cent by 2008-09. The Union Government achieved this target in

2007-08, with the fiscal deficit declining to 2.5 per cent of GDP. However, in

2008-09 the Union Government undertook several fiscal expansionary measures

such as revision of pay scales based on the recommendations of the Sixth Pay

Commission, waiver of farm loans and the expansion of the Mahatma Gandhi

National Rural Employment Guarantee Act (MGNREGA) to all districts from the 200

districts it was originally slated to cover. In addition, oil prices escalated

sharply, leading to a rise in subsidy. As a consequence of all this as well as

the global crisis, the fiscal deficit of Union Government increased to 6 per

cent in 2008-09 and 6.5 per cent in 2009-10.

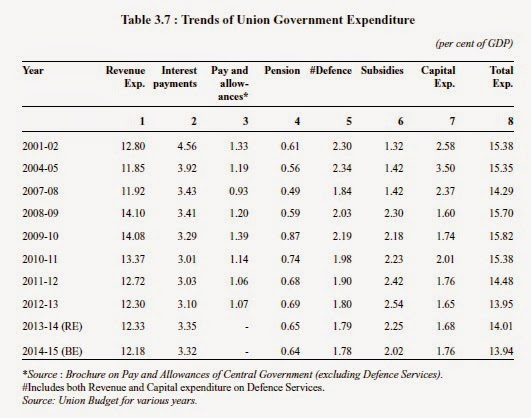

3.38 The share of

capital expenditure in the total expenditure of the Union Government declined

from 22.8 per cent in 2004-05 to 10.2 per cent in 2008-09 and has remained in

the range of 11 per cent to 13 per cent since then. Correspondingly, the

revenue expenditure increased to 89.8 per cent in 2008-09, and thereafter

declined only marginally, despite expenditure tightening measures. As a ratio

of GDP, the revenue expenditure of the Union Government increased from 11.9 per

cent in 2004-05 to 14.1 per cent in 2009-10 and is estimated at 12.2 per cent

in 2014-15 (BE). The major components of revenue expenditure comprising

subsidies, interest payments, defence expenditure, pay and allowances and

pensions are briefly analysed in the following paragraphs.

Major Subsidies

: Pay and Allowances and Pensions

3.46 Pay and

allowances of Union Government employees more than doubled between 2007-08 and

2011-12, from Rs.74, 647 crore to Rs.166, 792 crore due to the implementation of

the Sixth Central Pay Commission recommendations( Including Defence Services).

As a ratio of GDP, it jumped from a little over 0.9 per cent in 2007-08 to 1.2

per cent in 2008-09 and about 1.4 per cent in 2009-10 on account of both pay

revision and payment of arrears. However, it moderated to a little over 1 per

cent in 2012-13.

3.47 As in the case of

salaries, expenditure of the Union Government on pensions, which had declined

to less than 0.5 per cent of GDP in 2007-08, increased to about 0.9 per cent of

GDP in 2009-10 due to the impact of revision in pensions. Subsequently, it came

down to 0.7 per cent in 2010-11 and is estimated at 0.6 per cent in 2014-15

(BE).

3.48 Expenditure on

salary, pensions and interest payments together accounted for 5.67 per cent of

GDP in 2004-05 but declined marginally to 5.56 per cent of GDP in 2009-10, with

the rise in expenditure on salaries and pensions being more than compensated by

the decline in interest expenditure. These expenditures declined further to 4.9

per cent of GDP in 2012-13.

Revenue Expenditure

: Pensions

6.34 Pensions are

another committed liability which has been fully provided for in our

assessment. The assessment of pensions is based on the growth rate of pension

expenditure obtained from past data. The year-on-year growth of pension

expenditure has shown volatility, with growth declining to a low of 0.42 per

cent in 2002-03 and increasing to a high of 70.46 per cent in 2009-10. Given

these fluctuations, it is not appropriate for us to take a long-run trend

growth rate for this expenditure as a norm for assessment. It would be more

appropriate to use the observed growth in the recent past. However, a potential

fiscal liability may arise in the future with the introduction of the ‘one rank

one pension scheme’ for Defence Services. The Budget 2014-15 has also made an

additional allocation for this scheme, which is reflected in the increase in

the growth of pension expenditure to10.67 per cent over the 2013-14 (revised

estimates) growth of 6.62 per cent. While the Ministry of Finance projects an

increase in pension payments by 8.7 per cent in 2015-16, a 30 per cent increase

is expected in 2016-17 on account of the impact of the Seventh Pay Commission,

followed by an annual growth rate of 8 per cent in subsequent years. Pension

expenditures between 2011-12 and 2014-15 have grown on a year-on-year basis at

the rate of 9.35 per cent per annum. We are of the view that annual revisions

in the Dearness Allowance and annual accretions in the number of pensioners and

the corresponding pension obligations can be covered by this growth in pension

expenditure during our assessment period.

Defence Revenue Expenditure

6.35 Revenue

expenditure on defence has grown at an annual rate of 11.21 per cent between

2001-02 and 2012-13 and at the rate of 10.1 per cent between 2008-09 and

2012-13. In its submission to the Commission, the Ministry of Defence argued

that there has been a decline in the defence expenditure-GDP ratio over the

years and defence expenditure allocation in the Union budget needs to be

increased to expand the acquisition of arms and improve defence preparedness.

The Ministry pointed out that it has not been able to make necessary

procurements because of the constraint of funds and large amounts of committed

expenditure. The Ministry also mentioned that a substantial part of the defence

capital budget went into meeting committed expenditures. The Ministry of

Finance has also highlighted the need to increase defence outlays in order to

modernise and maintain defence assets and to finance defence acquisitions.

Accordingly, its projections have provided for an increase in defence revenue

expenditure (including salaries) of 30 per cent in 2016-17 which will

incorporate the Pay Commission impact, with a stable growth rate of 20 per cent

per annum in the remaining years.

Fiscal Consolidation:

Assessment and Issues

14.48 Our review shows

that, at an aggregate level, States made significant improvements in complying

with the FRBM targets prescribed by the FC-XII and FC-XIII. In the pre-crisis

period, fiscal consolidation at the State level was aided by a number of

factors, including implementation of state-level fiscal responsibility acts,

debt waiver and restructuring recommended by Finance Commissions, and

improvement in revenues on account of buoyancy of Central taxes and

introduction of value-added tax (VAT) at the state level. Despite States

experiencing pressure on their fiscal balances in the post-crisis period due to

lower buoyancy of Central taxes and increased expenditure commitment due to the

implementation of the recommendations of Pay Commissions, they largely

continued to comply with the FRBM targets.

Pay and Productivity

17.23 Wages and

salaries constitute a significant portion of the committed liabilities of both

the Union and States. Periodic revisions based on the recommendations of the

Pay Commissions of the Union, with States following suit, have contributed to

rising revenue expenditure. For States in particular, the fiscal impact of a

pay revision is severe, as the share of salary expenditure in their total

revenue expenditure is substantially larger than in the case of the Union.

Arrears in pay and bi-annual releases of Dearness Allowance compound the

burden.

17.24 Technically, the

recommendations of a Central Pay Commission are only for Central Government

employees and States are not bound to follow suit. Indeed, up to the 1980s,

States constituted their own Pay Commissions and prescribed their own pay

scales, based upon their fiscal capacity. However, since the Fifth Central Pay

Commission, salaries and allowances in States have tended to converge with

those in the Union Government and since the Sixth Central Pay Commission,

almost all States have adopted the Union pattern of pay scales, albeit with

modifications.

17.25 An internal

study by the Commission brought out the fact that the Union Government’s

expenditure on pay and allowances (including expenditure for the Union

Territories) [2 Excluding productivity linked bonus/ad-hoc bonus, honorarium

and encashment of earned leave, and travel allowances] more than doubled for

the period 2007-08 to 2012-13, from Rs. 46,230 crore to Rs. 1,08,071 crore [If

salary of defence services is included, the corresponding figures will be Rs.

73,073 crore and Rs. 1, 84,711 crore].

This increase can be

largely attributed to the implementation of the Sixth Central Pay Commission

recommendations, evident from the per employee annual salary (excluding defence

salary) increasing from Rs. 1,45,722 to Rs. 3,25,820 over this period. Moreover,

the share of expenditure on pay and allowances in revenue expenditure (net of

interest payment, pensions and grants-inaid) increased from 11.8 per cent in

2007-08 to 13.1 per cent in 2012-13. The incidence of salary expenditure is

much higher in the States than in the Union. In 2012-13, the share of

expenditure on pays and allowances of all employees in the revenue expenditure

(net of interest payments and pensions) among the States ranged from 28.9 per

cent to 79.1 per cent. Per employee (for regular employees) salary in 2012-13

across States ranged between Rs. 2,12,854 and Rs. 5,49,345. Thus, the impact of

revisions in pay scales on fiscal positions is uniformly significant, though it

varies widely across States.

17.26 Given the

variations across States and the lack of knowledge about the probable design

and quantum of award of the Seventh Central Pay Commission, we believe that it

is neither feasible, nor practicable, to arrive at any reasonable forecast of

the impact of the pay revision on the Union Government or the States. Further,

any attempt to fix a number in this regard, within the ambit of our

recommendations, carries the unavoidable risk of raising undue expectations.

17.27 Our concern is

the likely impact on overall budgetary resources, particularly of the States,

once the recommendations of the Seventh Central Pay Commission are announced

and adopted by the Union Government. All States have asked us to provide a

cushion for the pay revision likely during our award period. The Union Government’s

memorandum has built, in its forecast, the implications of a pay increase from

2016-17 onwards. The recommendations of the Seventh Central Pay Commission are

likely to be made only by August 2015, and unlike the previous Finance

Commissions, we would not have the benefit of having any material to base our

assessments and projections and to specifically take the impact into account.

We have, therefore, adopted the principle of overall sustainability based on

past trends, which should realistically capture the overall fiscal needs of the

States.

17.28 In our view, on

matters that impact the finances of both the Union and States, policies ought

to evolve through consultations between the States and the Union. This is

especially relevant in the determination of pay and allowances, where a part of

the government itself, in the form of the employees, is a stakeholder and

influential in policy making. A national view, arrived at through this process,

will open avenues for the Union and States to make collective efforts to raise

the extra resources required by their commitment to a pay revision. More

importantly, it would enable the Union and States to ensure that there is a

viable and justifiable relationship between the demands on fiscal resources on

account of salaries and contributions to output by employees commensurate with

expenditure incurred. In this regard, we reiterate the views of the FC-XI for a

consultative mechanism between the Union and States, through a forum such as

the Inter-State Council, to evolve a national policy for salaries and emoluments.

17.29 Further,we would

like to draw attention to the importance of increasing the productivity of

government employees as a part of improving outputs, outcomes and overall

quality of services relatable to public expenditures. The Seventh Central Pay

Commission, has, inter alia, been tasked with making recommendations on this

aspect. Earlier Pay Commissions had also made several recommendations to

enhance productivity and improve public administration. Productivity per

employee can be raised through the application of technology in public service

delivery and in public assets created. Raising the skills of employees through

training and capacity building also has a positive impact on productivity. The

use of appropriate technology and associated skill development require

incentives for employees to raise their individual productivities. A Pay

Commission’s first task, therefore, would be to identify the justify mix of

technology and skills for different categories of employees. The next step

would be to design suitable financial incentives linked to measurable

performance. We recommend the linking of pay with productivity, with a

simultaneous focus on technology, skills and incentives. Further, we recommend

that Pay Commissions be designated as ‘Pay and Productivity Commissions’,with a

clear mandate to recommend measures to improve ‘productivity of an employee’,

in conjunction with pay revisions. We urge that, in future, additional

remuneration be linked to increase in productivity.

Pensions

17.30 Pensions have been growing steadily, and the liability for pension

payments is likely to cast a very heavy burden on budgets in the coming years.

Some of the factors contributing to this growth are: (i) the rise in pensions

recommended by successive Pay Commissions; (ii) removal of the distinction

between people retiring at different points of time, so that all pensioners are

treated alike in their pension justifys; (iii) taking over the liability for

pensions of retired employees of aided institutions and local bodies; and (iv)

increasing longevity. The New Pension Scheme (NPS), a contribution-based scheme

introduced by the Union Government in 2004 for all new recruits after the

cut-off date, has now been adopted by all States, with the exception of West

Bengal and Tripura. This scheme has the merit of transferring future

liabilities to the New Pension Fund and factoring the current liability on a

State’s contribution from its current revenues. We urge States which have not

adopted the New Pension Scheme so far to immediately consider doing so for

their new recruits in order to reduce their future burden.

Conclusion: – The recommendations of 14th

Finance Commission are important for 7th Pay Commission. As the recommendations

of 14th FC is applicable with effect from 01.04.2015 the impact of above

mentioned recommendations will be the part of 7th CPC. Need not to say that 7th

CPC has the challenge to prepare the report in stipulated time including the

views of 14th FC.

Source Document:

http://finmin.nic.in/14fincomm/14fcreng.pdf

{kind=link}